Published on September 23, 2020 on The Edge Markets

Written by: Kamarul Azhar

ALREADY the world’s largest producer of certified sustainable palm oil (CSPO), Sime Darby Plantation Bhd (SDP) will continue with its sustainability drive, which includes not acquiring more plantation land.

Thus, growth will have to come from higher productivity of its plantations and offering more differentiated products from its downstream business Sime Darby Oils Sdn Bhd (SDO), says SDP chief financial officer Renaka Ramachandran.

And the downstream business is where the group’s growth story is.

“The reason is, if we are not going to expand via acreage — yes, we are going to expand via production — where is our profitability going to grow? Where’s our growth story? So our growth story is with SDO,” she says.

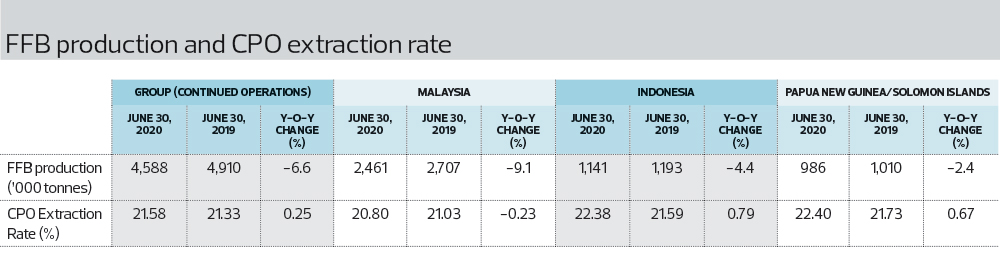

To grow productivity and profitability without acreage expansion, SDP has outlined several targets to be achieved by 2023. In the upstream segment, it aims for an average oil extraction rate (OER) of 23% by 2023. This compares with 21.58% as at June 30, 2020.

Yield per hectare is also targeted to reach 23 tonnes by 2023, says Renaka.

For SDO, the group has targeted for the downstream business to contribute 20% to its overall profitability by 2023. The profit contribution will eventually grow to 40% by 2025, she says.

SDP is confident that it will be able to achieve these targets, especially the 20% profit contribution from SDO by 2023. According to Renaka, the target will be exceeded by then, as the business is already making between 12% and 14% gross profit margins.

The first phase of SDP’s strategy will be to use its assets to its best capacity such as implementing new technology at its mills to reach higher OER and increase the contribution from differentiated products rather than from bulk selling.

“Instead of selling crude olein by bulk, which is dictated by market price, why don’t I put into a jerry can, for example, which is really the next basic step, and sell it to Africa, because I am going to earn US$10 (RM41.70) extra.

“So, [we] chase every dollar, if it means enhancement to the profits, but [we] try to do it all within our current sites right now. The plan is not to buy refineries all over the world because there is an SDO expansion. It is changing your own products into a differentiated product,” says Renaka.

Besides updating mill technology, SDP is also replanting its plantations with its own higher-yielding seedlings. SDP has invested more than RM150 million in research and development of the new seedlings called GenomeSelect.

The GenomeSelect seedlings produce 20% more crude palm oil than the next best available seedlings, claims SDP. The new seedlings will be able to produce CPO equivalent of of SDP’s plantations replanted, says Renaka, if only 4% of its plantations were replanted with them.

Every year, SDP spends RM700 million to RM800 million on replanting. It aims to replant at least 4% of its plantation land every year. For ageing plantations such as those in Indonesia, SDP replants between 5.5% and 7% of the total acreage annually, says Renaka.

“Our current replanting that we started in 2018 will start to provide an uplift in CPO production in five years’ time. We will have enough materials for all our replanting needs by 2022,” she says.

The use of GenomeSelect is also part of SDP’s efforts to drive a deforestation-free oil palm plantation industry.

On June 11, SDP said it had made public the genome sequence of its advanced seedling so that research centres and other major industry players could fast-track their work on improving yield.

Renaka was the group’s external auditor before taking up the role of CFO in 2011. In her time with SDP, she has seen the growth and opportunities of the downstream business.

She recalls that, in 2012, the lossmaking downstream business was a drag on SDP — then a subsidiary of Sime Darby Bhd — owing to high CPO prices. This is because high CPO price puts pressure on the margins of downstream business, especially when the products are commoditised.

In the financial year ended June 30, 2018, SDO contributed RM267 million, or 10.5%, to SDP’s profit before interest and tax (PBIT).

While the downstream business contributed 70% to SDP’s PBIT of RM406 million in the financial year ended Dec 31, 2019 (FY2019), Renaka says this should not be the gauge for SDO’s performance now, as CPO prices were in the doldrums then.

In the first half ended June 30, 2020 (1HFY2020), SDO posted PBIT of RM113 million, on the back of RM4.94 billion revenue, for a gross profit margin of 2.3%. The segment contributed 9.5% to the group’s pre-tax profit during the period.

The low margins of the downstream business is what SDP plans to address by selling more differentiated products to its customers globally. According to Renaka, profit margins of differentiated products could be as high as 30%.

Once SDP reaches its target of 20% profit contribution from the downstream business, it will consider how to further expand the business to achieve the 40% target by 2025.

“Post-2023, once we have everything in place, that is when we take the outward look in terms of expanding our business. So, then we look at further B2C — maybe, in some jurisdictions — or B2B expansions into new jurisdictions,” says Renaka.

Since SDP’s rebrand and launch of SDO in March last year, the group has pivoted towards producing more differentiated products, including its Natriéo nutraceutical brand. At the moment, SDO produces and markets tocotrienol — a vitamin E compound found in various vegetable oils including palm oil — under the Natriéo brand. This product has a high margin value, according to Renaka.

SDP has been producing tocotrienol since the 1990s, but it has yet to break into public acceptance as a health supplement. With the launch of the Natriéo brand by SDO, the group will be able to communicate directly with the public regarding the health benefits of tocotrienols.

“What we have done in recent years is largely to communicate the benefits of tocotrienols from a health perspective. We are also in the process of doing medical tests, but it is not completed yet,” says Renaka.

Shortage of foreign workers worrisome

The plantation industry is facing a labour crunch because of the Covid-19 pandemic. The border shutdowns have stopped the movement of foreign workers into the country, while some who are still here are looking to return to their home country.

For SDP, the group is short of around 2,500 workers, representing between 8% and 9% of its entire foreign workforce. This will affect the efficiency and productivity of its plantations in Malaysia.

“Not that the entire 2,500 are harvesters, but when you lose harvesters, production will decline and result in crop losses. I think the industry as a whole is going to face this more acutely in the second half of the year,” says Renaka.

She adds that the entire industry is looking at how it can address the situation via incentivising foreign workers to stay, as the Malaysian government has allowed them to stay on until at least year-end, to allow the oil palm industry to operate as it should.

“Perhaps, the next one or two months should indicate [the extent of the impact of the shortage of foreign workers]. Production numbers should give you an indication whether everything is hunky-dory.

“Now is actually meant to be the big period for oil palm production but, year on year, we are already lower,” she says.

While SDP can see itself sustaining its current level of production over the next three months by incentivising its workforce, the group is concerned about an extension of the border shutdown beyond 2020.

Renaka says the Covid-19 pandemic has pushed plantation companies to look at other ways to increase their production and reduce dependency on foreign workers, including employing more mechanisation in the estates.

“It is only now that there are investments being made for identifying innovative ways to increase oil yield scientifically. So, whether by controlled conditions or machinery assessments, it is only now that investments are being made,” she says.

Year to date, SDP’s share price has slipped about 7% to last Thursday’s price of RM5.06, giving it a market capitalisation of RM34.84 billion.

Reference:

https://www.theedgemarkets.com/article/sime-darby-plantation-banks-downstream-business-growth